Jobs, Rates, and This Week's Selloff

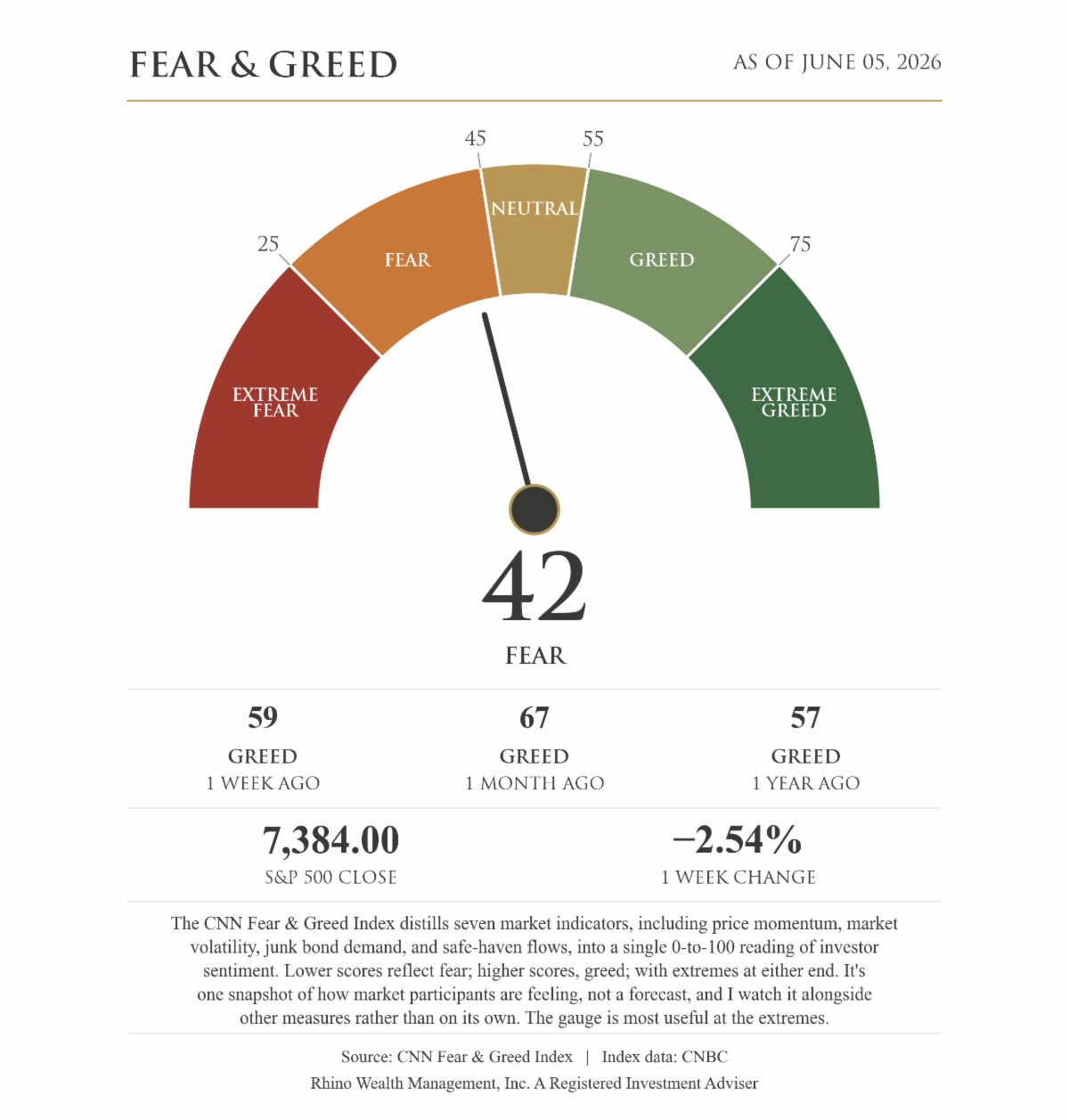

The S&P 500 finished the week down 2.54%, after nine consecutive weekly gains. Trees don't grow to the sky, and markets can have selloffs. There are two forces at play here, which are the topic of this week's newsletter.

This week we had a strong jobs report, which poured cold water on anyone still thinking the Fed was going to cut rates anytime soon. Also, money is rotating out of technology and chip stocks as market participants prepare for the historic Initial Public Offerings (IPOs) of SpaceX, Anthropic, and OpenAI. Index providers have changed their rules so companies this size can join the major indexes sooner than they used to, and when that happens the funds that track those indexes must buy the new shares. To buy stocks you need cash, so I suspect some of this selling is to raise cash to reallocate into these new issues. Later this year, if these stocks enter the indexes, it may push in the opposite direction from this week's selling.

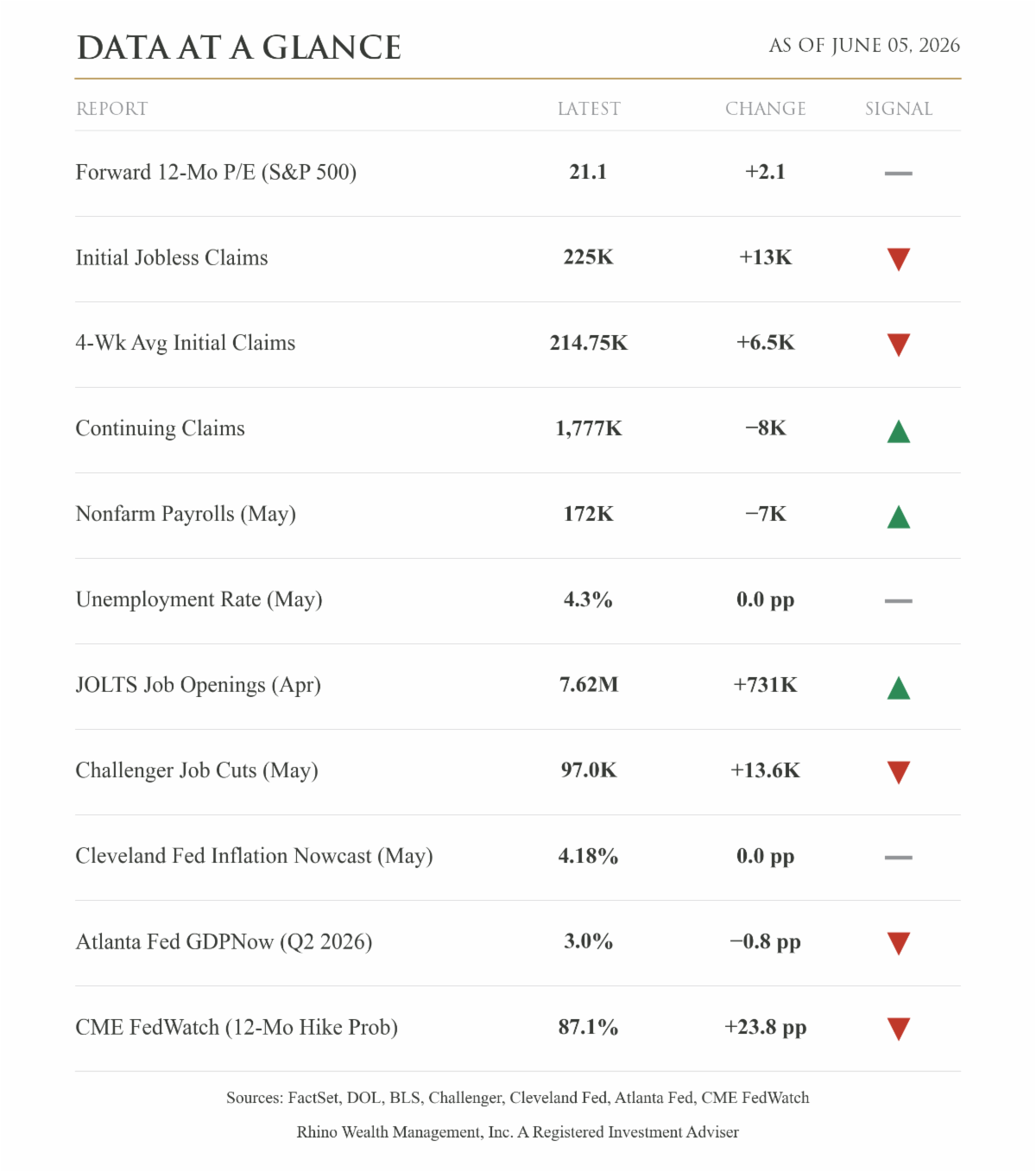

The jobs report showed that the economy added 172,000 jobs in May, more than double what forecasters expected, while unemployment held steady at 4.3%. The numbers for March and April were revised higher, and wage growth eased to 3.4% over the past year. Taken on its own, that's a strong report.

Underneath that headline, though, the picture is more mixed. Most of the new jobs came from a few steady sectors like restaurants, health care, and local government, while the higher-paying private industries were flat. The Job Openings and Labor Turnover Survey (JOLTS) shows fewer people quitting to take new positions, and the household survey shows those who lose a job are staying out of work longer. None of this signals a downturn, but together it describes a labor market that's slowly cooling but not weak.

The jobs number itself matters less than what the Fed does with the information. A labor market this steady, paired with inflation that's still running above the Fed's target, leaves little room to cut rates and puts a possible rate increase back in play. Markets are now pricing in roughly an 87% chance of a hike over the next 12 months. Add a new Fed Chair, Kevin Warsh, who took over last month, and the path ahead is genuinely uncertain. The President is pushing for lower rates, and the data does not support Fed easing. For now, a stronger economy is working against the possibility of rate cuts investors had been hoping for, and that tension is much of what moved markets this week.

The risk to plan around is rates staying higher for longer, not the economy weakening. What I'm watching is whether the labor market weakens or inflation eases. Either would give the Fed room to cut.

I'm following all of this closely, and nothing this week changes how I'm managing your portfolio. As always, reach out anytime with questions or concerns.

Glossary of Terms

Forward 12-Mo P/E (S&P 500) — How expensive stocks are relative to expected profits: the index price divided by analysts' earnings forecast for the next 12 months. Higher means investors are paying more per dollar of expected earnings. (FactSet)

Initial Jobless Claims — First-time filings for unemployment benefits in a week; a timely read on layoffs. Rising claims signal a softening job market. (DOL)

4-Wk Avg Initial Claims — A four-week average of initial claims that smooths weekly noise to show the trend. (DOL)

Continuing Claims — People still collecting benefits after their first week; reflects how hard it is for the unemployed to find new work. (DOL)

Nonfarm Payrolls — Net jobs added or lost across the economy in a month; the headline hiring measure. (BLS)

Unemployment Rate — Share of the labor force actively looking for work but without a job. (BLS)

JOLTS Job Openings — Total unfilled openings at month-end; a gauge of labor demand. (BLS)

Challenger Job Cuts — Layoffs announced by U.S. employers during the month. Rising cuts point to softening hiring plans. (Challenger, Gray & Christmas)

Cleveland Fed Inflation Nowcast — A daily model estimate of current-month CPI inflation (year-over-year) before the official figure is released. (Cleveland Fed)

Atlanta Fed GDPNow — A running model estimate of current-quarter economic growth (real GDP, annualized), updated as data arrives. (Atlanta Fed)

CME FedWatch (12-Mo Hike Prob) — The market-implied probability, from fed funds futures, that the Fed's target rate will be higher 12 months out than today. (CME Group)

Disclosure:

This material is provided by Todd Van Der Meid, MBA, CFP®, through Rhino Wealth Management, Inc., a Registered Investment Adviser, solely for informational purposes. It is not intended as investment, tax, legal, or accounting advice. Investors should consult qualified professionals before making financial decisions.

Opinions expressed herein are general in nature and not tailored to individual circumstances. Investment strategies discussed may not be suitable for every investor. All investments carry risk, including possible loss of principal, and past performance does not guarantee future results. No investment strategy or risk management technique ensures profit or eliminates risk in all market conditions.

Investments in foreign or emerging markets involve additional risk, such as currency fluctuations, geopolitical instability, and varying accounting standards. Sector-specific investments can be more volatile due to their concentrated nature. References to indexes are for illustrative purposes; indexes are unmanaged, cannot be invested into directly, and their performance does not reflect fees, expenses, or sales charges. Index performance is not indicative of specific investment performance.

Economic forecasts and forward-looking statements reflect current views and assumptions and are subject to change. Actual results may vary materially due to market or other conditions. There is no obligation to update forward-looking information.

Information presented herein comes from reliable third-party sources but is not guaranteed for accuracy or completeness. Rhino Wealth Management, Inc. disclaims liability for errors or omissions. Portions of this content may be generated using advanced analytical tools, including artificial intelligence, and all such content has been reviewed and validated by Todd Van Der Meid, MBA, CFP®, using proprietary quality-control measures. Rhino Wealth Management, Inc. does not directly hold securities; however, securities mentioned may be included within recommended portfolio models or held by clients. Please refer to our Form ADV for additional details regarding potential conflicts of interest.