In Spite of Everything

The S&P 500 closed the week at 7,575, a gain for the week of 1.23% in spite of headlines that supplied plenty of reasons to fall. The ceasefire with Iran broke down, the two sides are trading strikes again, and oil rose about 4% to close at $71.51 a barrel. Fed minutes showed a committee openly divided over whether rates should rise later this year, and June hiring came in at 57,000 jobs, the softest month since February. Stocks sold off early in the week and made it all back, with technology leading while the Dow lagged. In response to the shifting data, I moved the portfolio models one step toward defense this week, a change I explain further down.

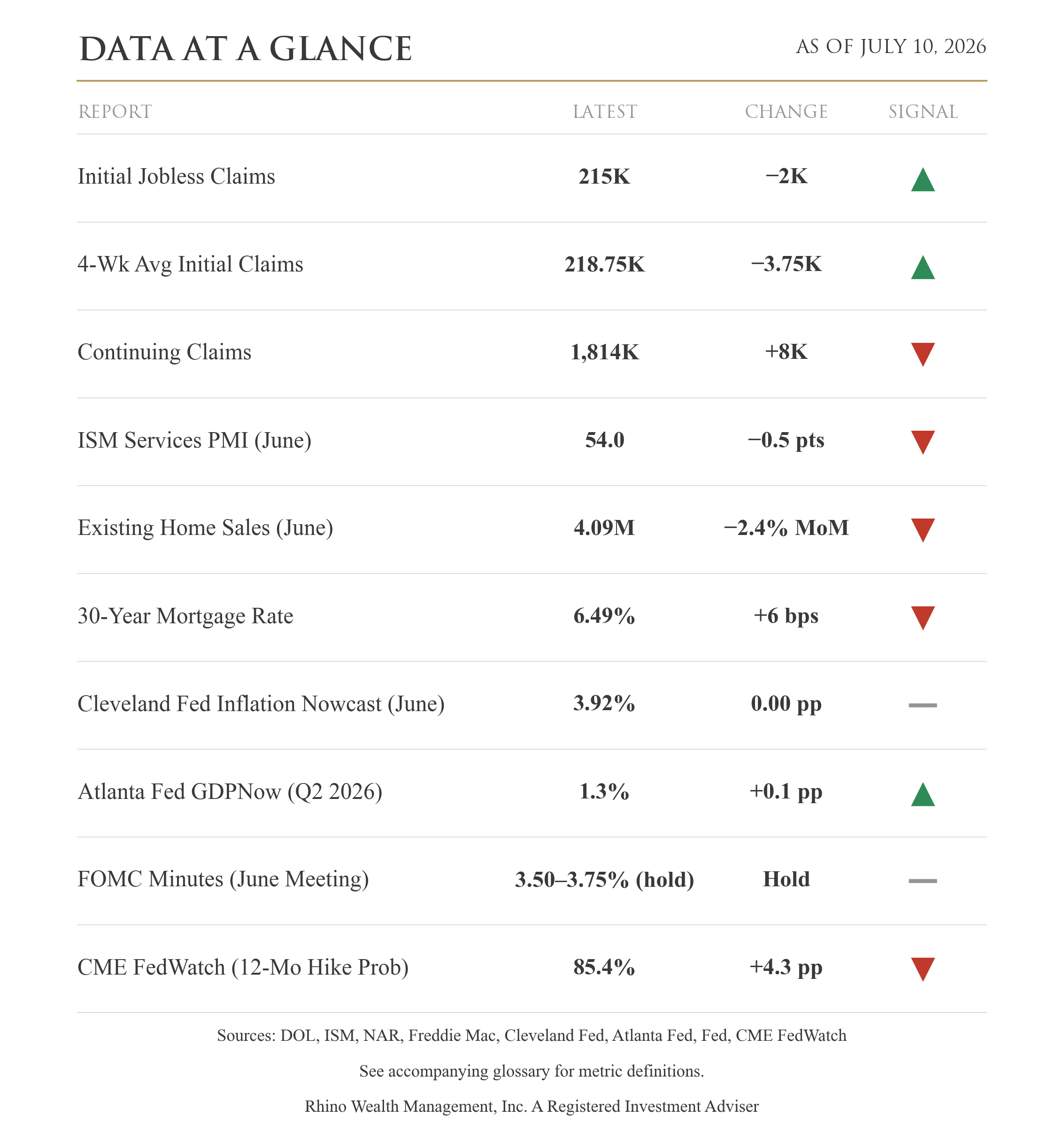

Let's start with the Fed, because it touches everything else. Minutes from the June meeting, released Wednesday, showed policymakers split three ways on where rates should end the year: nine expect at least one hike, eight expect no change, and one expects a cut. They also raised their forecast for the Fed's preferred inflation gauge to 3.6% for 2026, up from 2.7% just three months earlier. Futures traders now put the odds of a hike within the next year at 85%, up more than four points this week. A year ago the conversation was about cuts. I'm not penciling in lower rates anytime soon, and borrowers shouldn't either; the average 30-year mortgage ticked up to 6.49% this week.

A few weeks ago I wrote that I was hopeful about the ceasefire but not convinced, and this week made the case for not convinced. Energy is the main channel where the war reaches your portfolio: oil feeds inflation, and inflation is what has the Fed leaning hawkish. That's why a diplomatic headline can move markets more than an economic report does.

The economic data was steadier than the headlines. New claims for unemployment benefits fell to 215,000, low by any historical measure. But continuing claims, people still collecting benefits because they haven't found new work, sit at about 1.8 million and have been drifting higher since spring. That squares with June's hiring report: employers added just 57,000 jobs. Layoffs are still rare, but hiring has slowed, and people who are between jobs are staying there longer. Nothing in those numbers says trouble today; the trend is the part to watch. Services, which make up most of the economy, kept growing: a widely followed monthly survey of service businesses came in at 54.0, and anything above 50 means expansion. Existing home sales fell 2.4% in June.

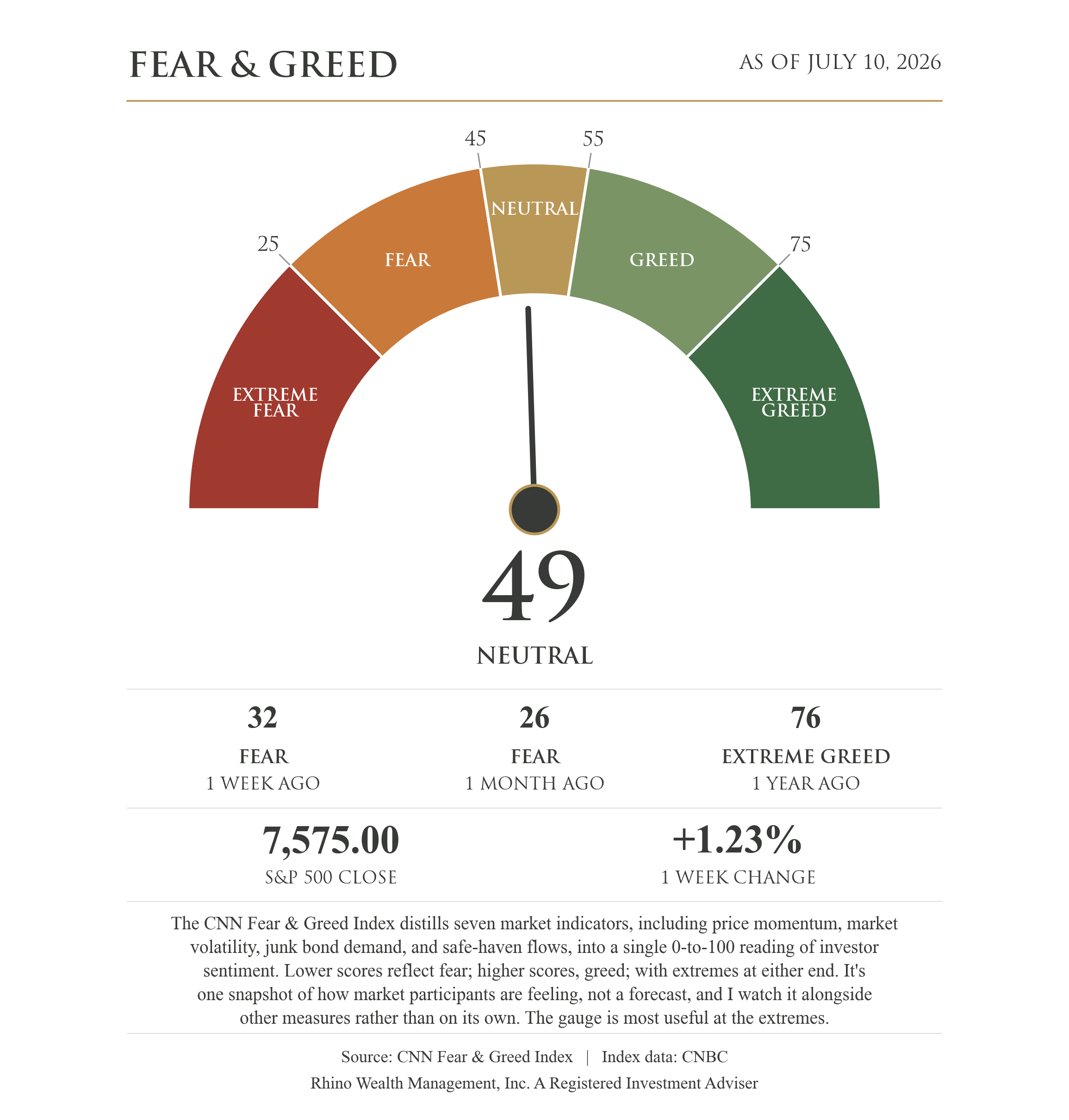

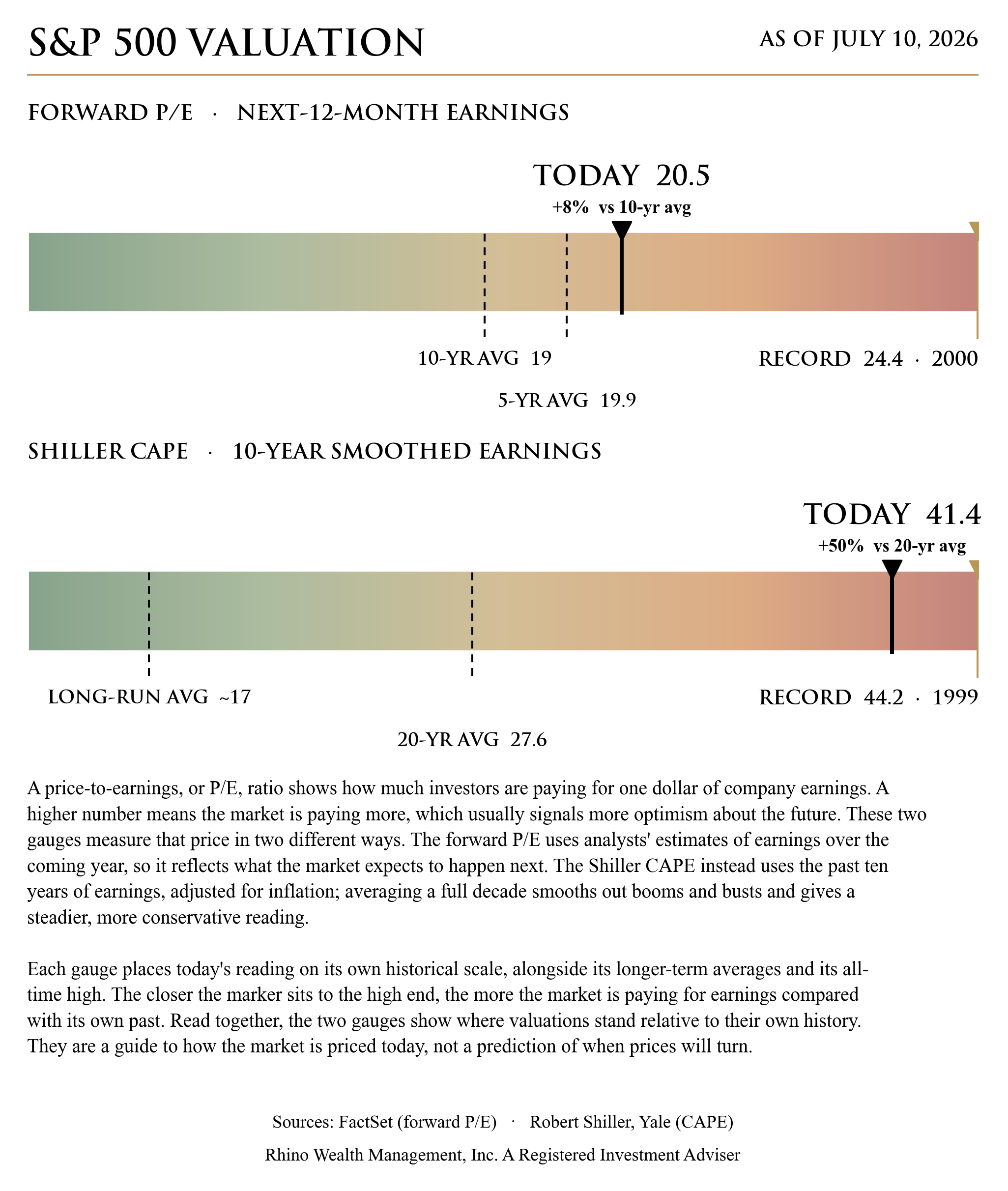

Investor sentiment recovered to 49 on CNN's Fear & Greed Index, a neutral reading, after sitting in fear at 32 a week ago. Valuations remain above their averages. Investors are paying about 20.5 times the earnings companies are expected to produce over the coming year, 8% above the 10-year average, and the Shiller CAPE, which averages ten years of inflation-adjusted earnings to smooth out booms and busts, is 50% above its 20-year average. The market is priced above its own history at the same time the Fed is leaning toward hikes and a conflict is back in the news. That combination doesn't leave much room for disappointment.

That backdrop is why I made an adjustment to the portfolio models this week. Alongside the ETF scoring system, my allocation process includes a macroeconomic overlay: a setting that tells the scoring system how much emphasis to place on defensive traits like quality and lower volatility versus aggressive ones like price momentum. I moved that setting one step toward defense, to a position I call Lean Risk Off. The reasons are the ones above: a broken ceasefire, inflation near 4%, a Fed whose bias now points toward raising rates rather than cutting them, and hiring that slowed sharply in June. Any one of those is manageable; together they argue for leaning on the steadier parts of the market over the next few months. Before making the change, I ran the same research assignment through four independent AI platforms, each drawing on its own sources, and reviewed the data myself. All four pointed to the same conclusion I reached. The models remain fully invested and globally diversified; nothing moved to cash. This is a shift in emphasis, and I'll move it back if the data improves, or further toward defense if it deteriorates.

What I'm watching from here: June's inflation report arrives Tuesday, the first hard read on prices since those Fed minutes, and the big banks open earnings season the same morning.

Disclosure:

This material is provided by Todd Van Der Meid, MBA, CFP®, through Rhino Wealth Management, Inc., a Registered Investment Adviser, solely for informational purposes. It is not intended as investment, tax, legal, or accounting advice. Investors should consult qualified professionals before making financial decisions.

Opinions expressed herein are general in nature and not tailored to individual circumstances. Investment strategies discussed may not be suitable for every investor. All investments carry risk, including possible loss of principal, and past performance does not guarantee future results. No investment strategy or risk management technique ensures profit or eliminates risk in all market conditions.

Investments in foreign or emerging markets involve additional risk, such as currency fluctuations, geopolitical instability, and varying accounting standards. Sector-specific investments can be more volatile due to their concentrated nature. References to indexes are for illustrative purposes; indexes are unmanaged, cannot be invested into directly, and their performance does not reflect fees, expenses, or sales charges. Index performance is not indicative of specific investment performance.

Economic forecasts and forward-looking statements reflect current views and assumptions and are subject to change. Actual results may vary materially due to market or other conditions. There is no obligation to update forward-looking information.

Information presented herein comes from reliable third-party sources but is not guaranteed for accuracy or completeness. Rhino Wealth Management, Inc. disclaims liability for errors or omissions. Portions of this content may be generated using advanced analytical tools, including artificial intelligence, and all such content has been reviewed and validated by Todd Van Der Meid, MBA, CFP®, using proprietary quality-control measures. Rhino Wealth Management, Inc. does not directly hold securities; however, securities mentioned may be included within recommended portfolio models or held by clients. Please refer to our Form ADV for additional details regarding potential conflicts of interest.