A quiet freeze in the job market

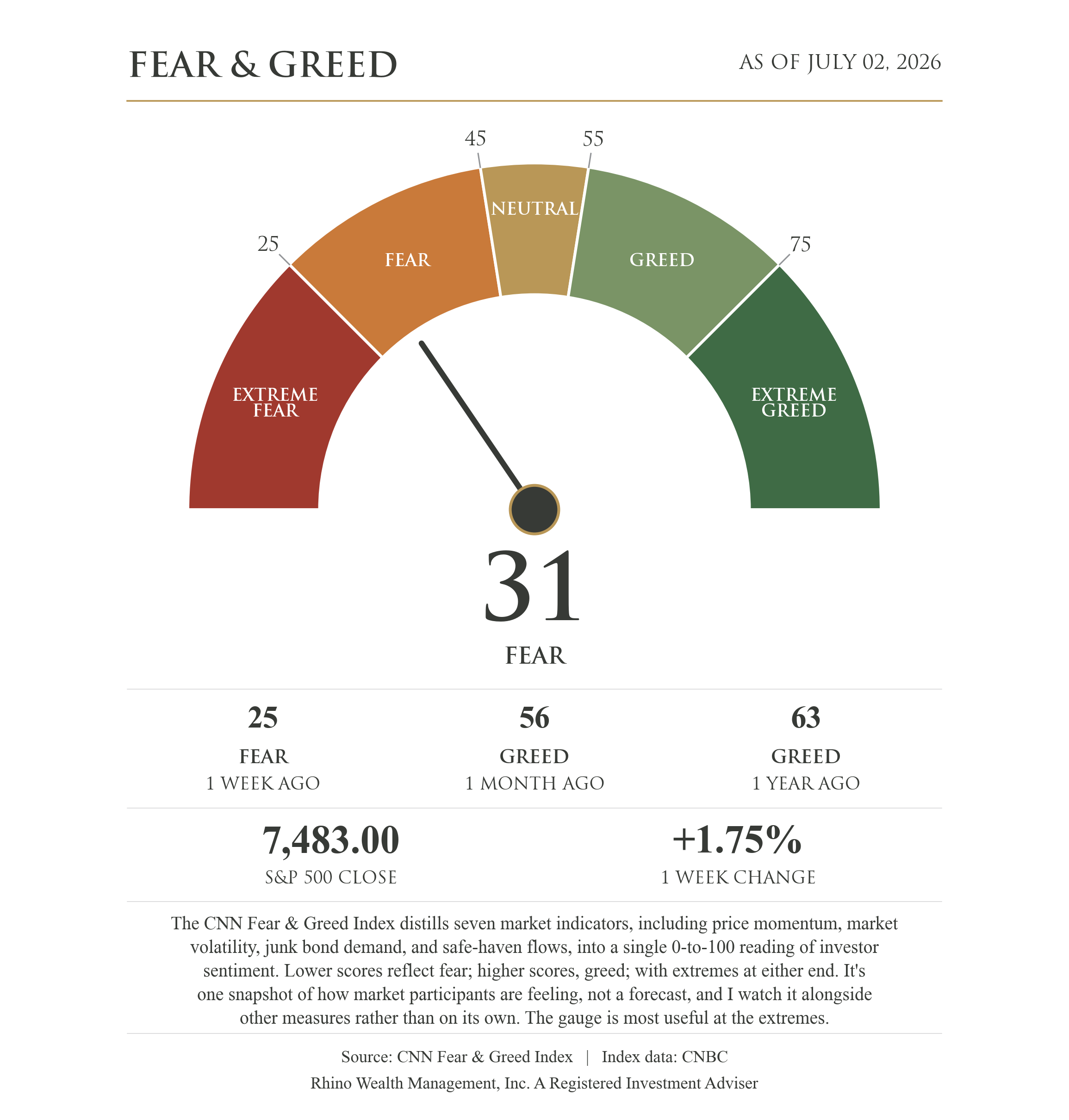

The S&P 500 finished the week up 1.75% at 7,483 while investors looked for direction. Fed Chair Warsh said consumers' expectations for inflation are coming down, an idea the Cleveland Fed's model reinforces. The market isn't as sure, still pricing a strong chance the Fed's next move is a hike. At the same time, the Atlanta Fed's model shows the economy may be slowing, and this week's employment data agrees, reflecting a stable to softening labor market. All while corporate earnings and markets remain resilient. In a week like this, everyone gets to be right about something.

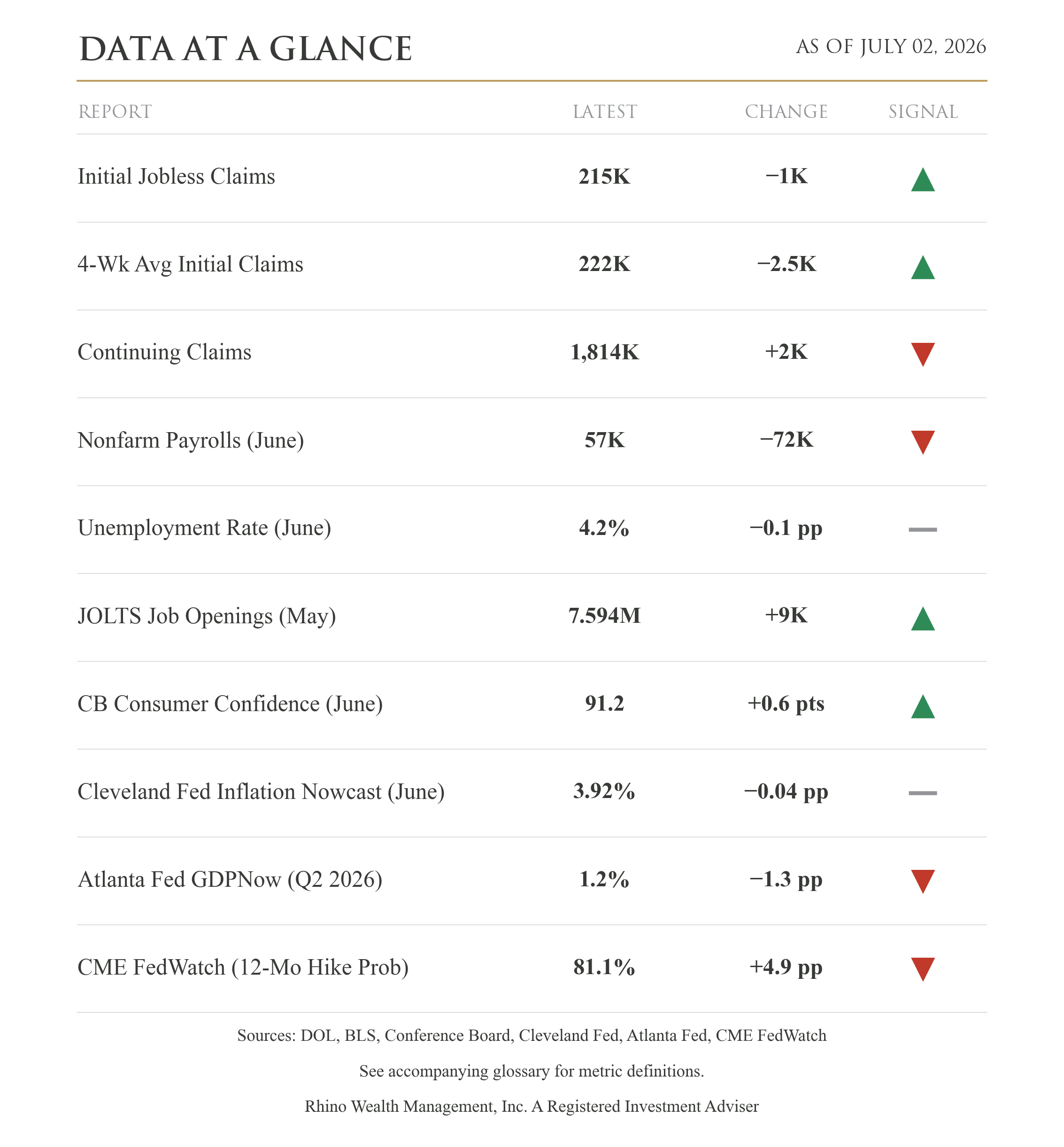

Thursday's June jobs report showed 57,000 new jobs, roughly half what economists expected and a sharp step down from May's 129,000. The prior two months were also revised down by a combined 74,000. The unemployment rate actually fell, from 4.3% to 4.2%, but for the least encouraging reason: the share of adults working or looking for work dropped to 61.5%, its lowest since early 2021. When fewer people are counted as looking, the rate can fall without anyone finding a job.

New claims for unemployment benefits came in at 215,000, a five-week low, and the four-week average eased to 222,000. Layoffs are still rare. But continuing claims, the count of people still collecting benefits because they haven't found the next job, rose to 1,814,000, the highest in three months, while job openings held steady at about 7.6 million. This is a job market that's frozen rather than falling apart. Employers aren't cutting, but they aren't hiring much either, and anyone who loses a job is waiting longer to land the next one. The Conference Board's consumer confidence survey says the same thing. The June index ticked up to 91.2, but the same survey found the share of Americans who say jobs are hard to get at its highest in five and a half years.

A cooling job market matters most for what it means at the Fed. Fewer paychecks mean less spending and less pressure on prices, which would normally argue against raising rates. The futures market reads it differently. It now puts the odds of a rate hike over the next year at 81%, up almost five points this week even after the weak jobs report. Investors appear to be betting that with inflation still near 4%, a slower job market won't be enough on its own to bring prices back in line.

There was no official inflation report this week, so the table uses the Cleveland Fed's nowcast, a model that estimates inflation in real time from daily data instead of waiting for the monthly release. It puts June at 3.92%, down from May's 4.2%, and its first look at July opens near 3.5%. If those readings hold, inflation peaked in May and is expected to step down through the summer. Two cautions before leaning on it: this is a model estimate, not a Fed forecast, and this early in the month the July figure is built mostly from gas prices. June's official number prints in mid-July and will tell us whether the peak is actually in.

The Atlanta Fed's running estimate of second-quarter growth has fallen from 3.0% in mid-June to 2.5% last week to 1.2% now. The best case is an economy that cools just enough to keep the Fed on hold while inflation drifts down on its own. The risk is that the economic slowing doesn't stop where we'd like it to. The next few weeks of data will start to tell us which one we're getting.

None of this yet reads like an economy in trouble. Layoffs remain low, and oil, which started this whole inflation episode, is back to roughly where it sat before the war began. If the nowcast is right, the squeeze on prices is starting to ease. What I'm watching from here: the mid-July inflation print, what the Fed does with all the data at its meeting at the end of the month, and any resurgence of geopolitical conflict.

Disclosure:

This material is provided by Todd Van Der Meid, MBA, CFP®, through Rhino Wealth Management, Inc., a Registered Investment Adviser, solely for informational purposes. It is not intended as investment, tax, legal, or accounting advice. Investors should consult qualified professionals before making financial decisions.

Opinions expressed herein are general in nature and not tailored to individual circumstances. Investment strategies discussed may not be suitable for every investor. All investments carry risk, including possible loss of principal, and past performance does not guarantee future results. No investment strategy or risk management technique ensures profit or eliminates risk in all market conditions.

Investments in foreign or emerging markets involve additional risk, such as currency fluctuations, geopolitical instability, and varying accounting standards. Sector-specific investments can be more volatile due to their concentrated nature. References to indexes are for illustrative purposes; indexes are unmanaged, cannot be invested into directly, and their performance does not reflect fees, expenses, or sales charges. Index performance is not indicative of specific investment performance.

Economic forecasts and forward-looking statements reflect current views and assumptions and are subject to change. Actual results may vary materially due to market or other conditions. There is no obligation to update forward-looking information.

Information presented herein comes from reliable third-party sources but is not guaranteed for accuracy or completeness. Rhino Wealth Management, Inc. disclaims liability for errors or omissions. Portions of this content may be generated using advanced analytical tools, including artificial intelligence, and all such content has been reviewed and validated by Todd Van Der Meid, MBA, CFP®, using proprietary quality-control measures. Rhino Wealth Management, Inc. does not directly hold securities; however, securities mentioned may be included within recommended portfolio models or held by clients. Please refer to our Form ADV for additional details regarding potential conflicts of interest.