From Cuts to Hikes

The S&P 500 finished the week lower, pressured by a Fed that turned more hawkish, a hot inflation report, and a U.S.-Iran ceasefire that may be shaky.

Coming into this year, the debate was about how many times the Fed would cut rates. After its latest meeting, the question is whether the Fed's next move is a hike. The reason showed up in the latest inflation report.

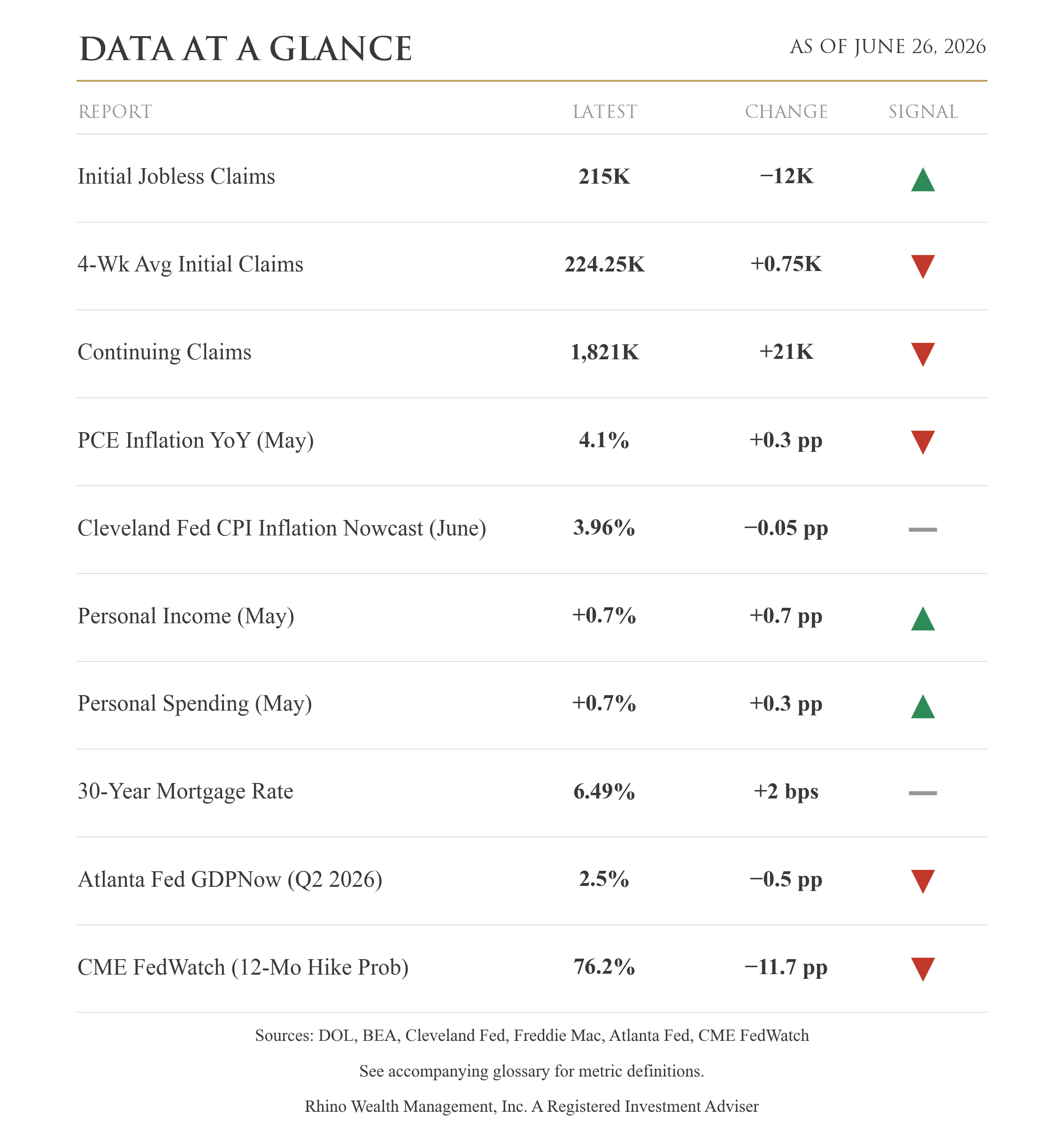

The latest Personal Consumption Expenditures (PCE) report, the Fed's preferred inflation gauge, rose again over the past year, to its highest in years. Even if we strip out food and energy, which we know have been inflation drivers, the core trend, the one the Fed leans on, was still rising. Inflation isn't drifting back down toward where the Fed wants it. It's moving the other way.

Here's what's fueling it: you and me. Incomes are rising, and so is spending, both more than expected. People are still earning and still spending. Consumer spending fuels economic growth, but too much consumer demand keeps inflation sticky. The way the cycle works is that the Fed raises rates to cool demand and bring inflation down. In past cycles the Fed has raised too much and cooled the economy into recession. So, we have to pay close attention to where the whole committee stands.

At Fed Chair Kevin Warsh's first meeting, the committee held rates steady, which everyone expected. The surprise was in the projections. Their own forecasts now point to higher rates by the end of the year, not lower, and more members expect a rate increase than a cut. They also nudged up their outlook for inflation. A few months ago, this group expected to be cutting by now. Now they're talking about raising rates instead.

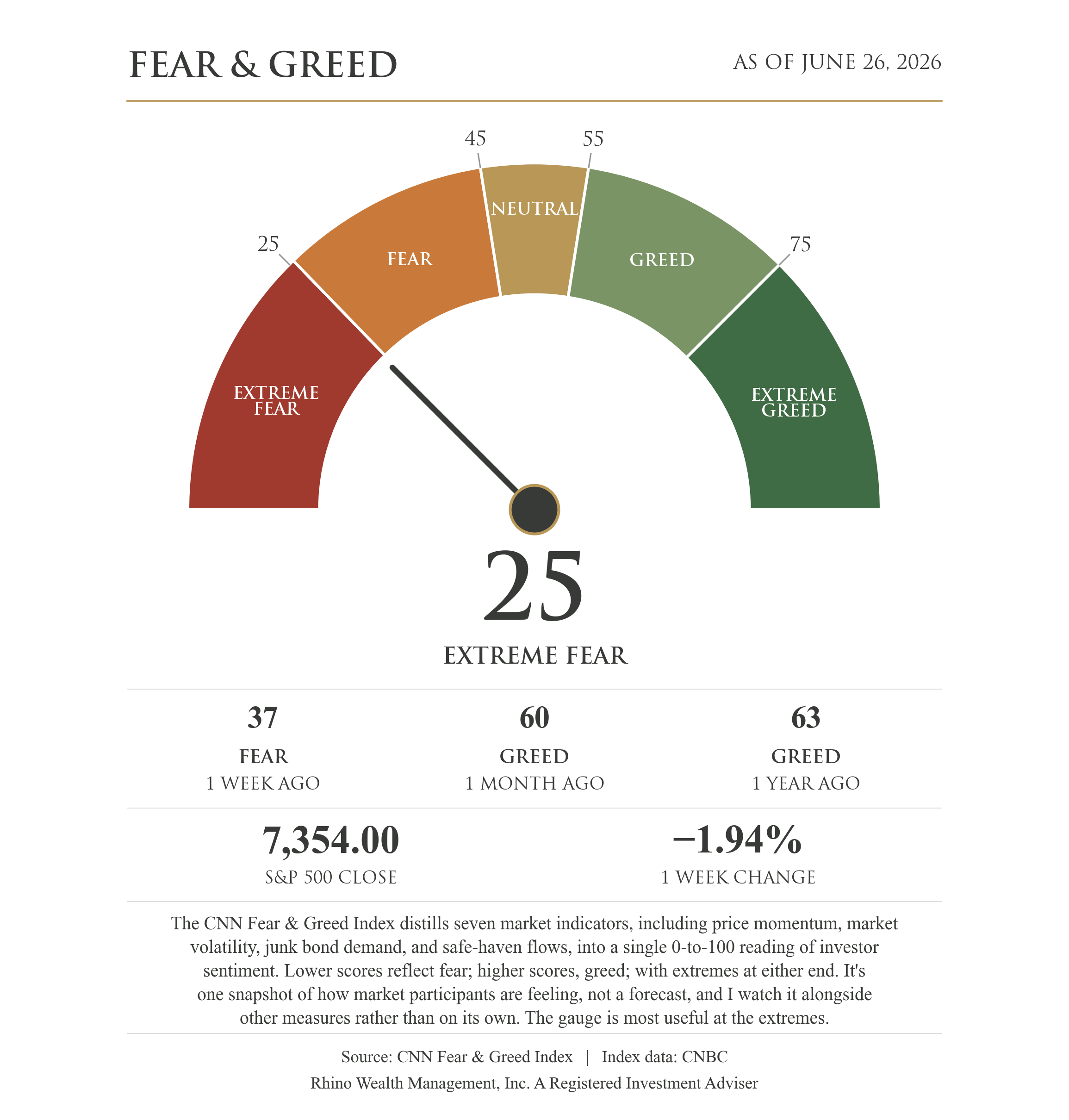

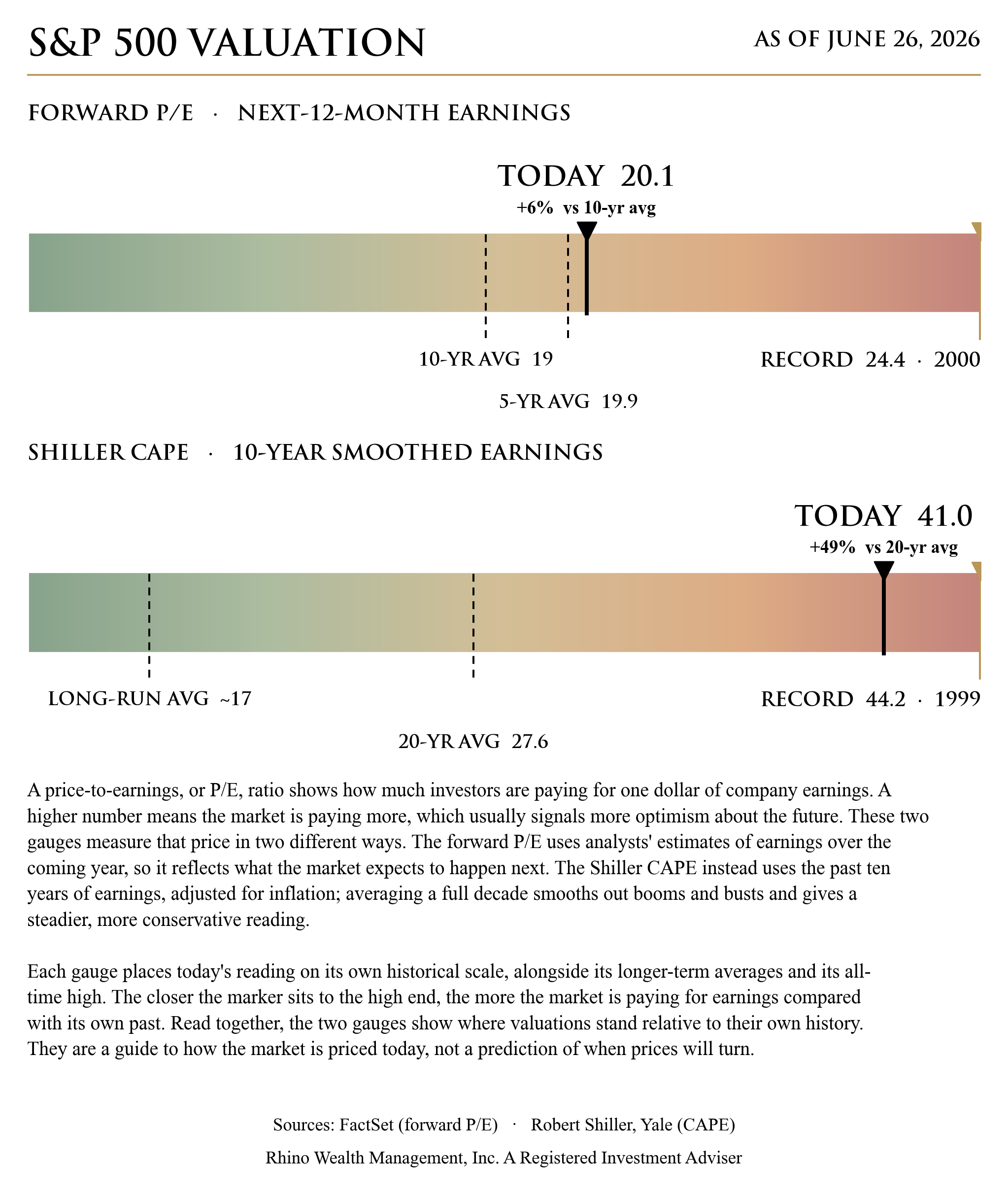

For most of the year, the market shrugged all of this off and kept pushing to new highs. That has started to crack. Stocks have pulled back from their records, and the Fear & Greed Index, which gauges investor mood on a scale from extreme fear to extreme greed, has dropped well into fear. The hot inflation report is a big part of why. If prices keep climbing and the Fed leans toward hikes, a market priced this high doesn't leave much room if things go wrong.

Then there's Iran. A peace deal reached just this month took the threat of an oil-supply shock off the table, which helped calm markets. That calm is already in question. Iran launched drones at a cargo ship in the Strait of Hormuz, the narrow passage much of the world's oil moves through. President Trump called the attack a violation of the ceasefire. He hasn't said how the United States will respond, and trouble like this has a way of escalating over a weekend, so I'm staying alert. If it spreads, oil and inflation could climb again, which is the last thing the Fed wants right now.

Growth, meanwhile, is quietly losing steam. The Atlanta Fed's running estimate of the economy has slipped, pointing to a slower pace than a few months ago. It's still healthy, but it's cooling just as inflation heats up, which is the opposite of what the Fed would want. It doesn't change the picture today, but it's the imbalance to watch as the year goes on.

The rate cuts that markets were counting on this year aren't coming. The economy is healthy enough that it doesn't need them. What's new is the idea of hikes, which almost no one expected coming into the year, and investors are still getting used to it. The market's gains this year are built on real earnings, the economy is still growing and still adding jobs, and a pullback with a jump in fear is how markets adjust to new information. In the coming weeks I'll be watching for any signals about how quickly rates might rise, and for any further trouble in the Middle East.

Glossary of Terms

Initial Jobless Claims — The number of people who filed for unemployment benefits for the first time in the past week. It's one of the timeliest signals of layoffs and labor-market health. Source: U.S. Department of Labor.

4-Week Average Initial Claims — The four-week moving average of initial claims. Averaging the weekly figures smooths out one-week noise and shows the underlying trend more clearly. Source: U.S. Department of Labor.

Continuing Claims — The number of people still receiving unemployment benefits after their first claim. It reflects how quickly people who lost jobs are finding new ones. Source: U.S. Department of Labor.

PCE Inflation YoY (May) — The year-over-year change in the Personal Consumption Expenditures price index, the inflation measure the Federal Reserve watches most closely. Source: Bureau of Economic Analysis.

Cleveland Fed CPI Inflation Nowcast (June) — A real-time estimate of where Consumer Price Index (CPI) inflation is tracking for the current month, before the official reading is published. It offers an early sense of inflation's direction. Source: Federal Reserve Bank of Cleveland.

Personal Income (May) — The month-over-month change in total income households receive from wages, investments, and other sources. It gauges Americans' capacity to spend and save. Source: Bureau of Economic Analysis.

Personal Spending (May) — The month-over-month change in what households actually spend. Consumer spending is the largest driver of U.S. economic growth. Source: Bureau of Economic Analysis.

30-Year Mortgage Rate — The average interest rate on a 30-year fixed-rate home loan. It's a key measure of housing affordability and a barometer of broader borrowing costs. Source: Freddie Mac Primary Mortgage Market Survey.

Atlanta Fed GDPNow (Q2 2026) — A model-based running estimate of current-quarter economic growth that updates as new data arrive, providing an early read before official GDP is released. Source: Federal Reserve Bank of Atlanta.

CME FedWatch (12-Mo Hike Prob) — The market-implied probability, derived from fed funds futures, that the Federal Reserve's target rate will be higher roughly twelve months from now. It shows how much additional rate tightening investors are pricing in. Source: CME FedWatch Tool.

Disclosure:

This material is provided by Todd Van Der Meid, MBA, CFP®, through Rhino Wealth Management, Inc., a Registered Investment Adviser, solely for informational purposes. It is not intended as investment, tax, legal, or accounting advice. Investors should consult qualified professionals before making financial decisions.

Opinions expressed herein are general in nature and not tailored to individual circumstances. Investment strategies discussed may not be suitable for every investor. All investments carry risk, including possible loss of principal, and past performance does not guarantee future results. No investment strategy or risk management technique ensures profit or eliminates risk in all market conditions.

Investments in foreign or emerging markets involve additional risk, such as currency fluctuations, geopolitical instability, and varying accounting standards. Sector-specific investments can be more volatile due to their concentrated nature. References to indexes are for illustrative purposes; indexes are unmanaged, cannot be invested into directly, and their performance does not reflect fees, expenses, or sales charges. Index performance is not indicative of specific investment performance.

Economic forecasts and forward-looking statements reflect current views and assumptions and are subject to change. Actual results may vary materially due to market or other conditions. There is no obligation to update forward-looking information.

Information presented herein comes from reliable third-party sources but is not guaranteed for accuracy or completeness. Rhino Wealth Management, Inc. disclaims liability for errors or omissions. Portions of this content may be generated using advanced analytical tools, including artificial intelligence, and all such content has been reviewed and validated by Todd Van Der Meid, MBA, CFP®, using proprietary quality-control measures. Rhino Wealth Management, Inc. does not directly hold securities; however, securities mentioned may be included within recommended portfolio models or held by clients. Please refer to our Form ADV for additional details regarding potential conflicts of interest.